-

OCT 20, 2025

UNLOCKEDFinance General – BGA Policy 2026 Budget Snapshot

The finance general category is a budgetary catch-all for non-departmental spending. There is no dedicated budget hearing devoted specifically to finance general appropriations, although in recent years it has made up close to half of the city budget.

This snapshot has been provided for the first day of budget hearings, when the Budget Director and OBM staff will be present for a budget overview, offering the best opportunity for alderpersons to ask questions relating to finance general appropriations.

Departmental Highlights

Snapshot: Appropriation Changes from 2025 Budget

2025 Budgeted 2026 Proposed Net Change Percent Change Average Annual Rate of Change (2011-2025) Inflation-adjusted Rate of Change (2011-2024) Appropriations $8,065,669,719 $8,053,719,737 -$11,949,982 -0.15% 12.7% 8.1% - The proposed $12 million (-0.15%) reduction in finance general appropriations would be the first time since 2021 that finance general appropriations have declined from the previous year.

- The scheduled wage adjustments appropriation saw the largest net increase from the previous year in the 2026 budget proposal, up $209.4 million (117.3%) from the 2025 budget. (Recent police and fire contracts have substantially increased the city’s expected salary increases for some of its largest unions.)

- Outside contracting costs are up substantially within finance general, with the professional and technical services appropriation up $10.4 million (6.7%) from the previous year’s budget, and pass-through spending for delegate agencies up $18.6 million (1373.9%), all of the latter increase from the new Community Safety Fund proposed to be funded with a revived corporate head tax.

- The largest cuts to finance general appropriations from the previous year are in the advance pension payments, a cumulative -$293.3 across the four annuity and benefit funds. The advance payments have not been eliminated entirely, but are down substantial percentages ranging from -50.3% (policemen's fund) to -66.6% (laborers’ fund).

- In 2024, the most recent year for which full-year local fund actuals are available, Finance general actual and encumbered spend exceeded budgeted amounts in the city pension contribution, reimbursement of indirect costs to corporate fund, court settlement, and medicare tax contribution categories.

- A small number of finance general appropriations budgeted in 2024 generated no actual spend, including $4.2 million for operations and maintenance reserves, $3.3 million for pension payment reimbursements, and $2.2 million for interest.

Historical Context

Finance general is the section of the budget used for citywide or non-departmental expenses. In the city’s budget practices, this includes pension and benefit costs, which are not broken out by department or individual position, but are instead treated as lump-sum appropriation accounts within finance general.

(The only exception to this practice is in the budget department’s calculation of mandatory funding minimums for the Office of Inspector General, Civilian Office of Police Accountability, and Community Commission for Public Safety and Accountability. For purposes of meeting those funding floors only, OBM estimates a “fringe” value of pension and benefit costs and counts them towards the minimum. A recent BGA Policy analysis explores the impact of this exception to the normal handling of pension/benefit costs in more depth.)

The finance general category has grown over time, both as a percentage of the overall budget and in terms of how many unique appropriations are contained within the finance general section of the budget. Because pension and benefit costs are lumped together under finance general (and are among the city’s largest expenses), this section of the budget began to increase more dramatically starting in 2015 with the onset of state-mandated “pension ramp” payments, and again in 2020 and 2022 as ramp payments shifted to actuarially-calculated payments.

Historically, the finance general budget as a whole has increased by an average of 12.7% annually, or 8.1% adjusted for inflation, compared to a citywide average rate of 8.3% (inflation-adjusted 4.4%).

The proposed 2026 budget includes a $12 million reduction in finance general appropriations from 2025’s budget. Although a very slight reduction as a percentage of finance general appropriations (-0.15%), the change would be the first time since 2021 that finance general appropriations have declined from the previous year.

Over the past three complete budget years for which local fund actuals/encumbrances data is available, the city spent on average 80.8% of its finance general budget, compared to the citywide average 86.4% local fund spend.

Appropriations

Finance general appropriations are entirely locally-funded in this year’s budget proposal, as in the previous year. The non-departmental budget section draws from a wide range of funds, with the general purpose Corporate Fund making up the largest share at 27.1% of finance general’s funding.

Fund 2025 Budgeted 2026 Proposed Net Change from 2024 Percent Change from 2025 Percent of 2026 Funding Corporate Fund $2,117,197,528 $2,185,110,953.00 $67,913,425 3.2% 27.1% Chicago O'Hare Airport Fund $1,134,500,174 $1,159,587,986.00 $25,087,812 2.2% 14.4% Policemen's Annuity and Benefit Fund $1,142,480,593 $1,106,262,515.00 -$36,218,078 -3.2% 13.7% Municipal Employees' Annuity and Benefit Fund $1,131,544,851 $1,046,708,718.00 -$84,836,133 -7.5% 13.0% Water Fund $537,901,015 $520,111,634.00 -$17,789,381 -3.3% 6.5% Firemen's Annuity and Benefit Fund $474,003,222 $461,787,994.00 -$12,215,228 -2.6% 5.7% Bond Redemption and Interest Series Fund $417,653,349 $430,103,270.00 $12,449,921 3.0% 5.3% Sewer Fund $335,326,182 $327,569,173.00 -$7,757,009 -2.3% 4.1% Chicago Midway Airport Fund $192,029,764 $209,448,722.00 $17,418,958 9.1% 2.6% Laborers' and Retirement Board Annuity and Benefit Fund $158,505,705 $145,508,044.00 -$12,997,661 -8.2% 1.8% Library Note Redemption and Interest Tender Notes Series "B" Fund $122,026,000 $122,026,000.00 $0 0.0% 1.5% Vehicle Tax Fund $102,970,730 $106,509,659.00 $3,538,929 3.4% 1.3% CTA Real Property Transfer Tax Fund $59,327,255 $63,423,286.00 $4,096,031 6.9% 0.8% Emergency Communication Fund $50,539,729 $55,930,992.00 $5,391,263 10.7% 0.7% Library Fund $32,019,121 $34,344,498.00 $2,325,377 7.3% 0.4% Foreign Fire Insurance Tax Fund $25,309,000 $25,309,000.00 $0 0.0% 0.3% Community Safety Fund 0 $18,636,626.00 $18,636,626 New Fund 0.2% Special Events and Municipal Hotel Operators' Occupation Tax Fund $15,461,181 $18,181,596.00 $2,720,415 17.6% 0.2% Tax Increment Financing Administration Fund $6,392,847 $6,897,616.00 $504,769 7.9% 0.1% Motor Fuel Tax Fund $3,245,005 $3,026,000.00 -$219,005 -6.7% 0.0% Garbage Collection Fund $2,297,809 $2,641,263.00 $343,454 14.9% 0.0% Casino Community Benefits Fund 0 $2,000,000.00 $2,000,000 New Fund 0.0% Houseshare Surcharge - Homeless Services Fund $1,192,000 $973,241.00 -$218,759 -18.4% 0.0% Houseshare Surcharge - Domestic Violence Fund $784,000 $494,621.00 -$289,379 -36.9% 0.0% Wheelchair Accessible Vehicle Fund $271,714 $389,069.00 $117,355 43.2% 0.0% Neighborhoods Opportunity Fund $323,905 $374,218.00 $50,313 15.5% 0.0% Affordable Housing Opportunity Fund $804,390 $299,766.00 -$504,624 -62.7% 0.0% Opioid Settlement Fund $40,177 $40,177.00 $0 0.0% 0.0% Cannabis Regulation Tax $1,513,238 $13,238.00 -$1,500,000 -99.1% 0.0% Vaping Settlement Fund $9,235 $9,235.00 $0 0.0% 0.0% Construction and Demolition Debris Management Fund 0 $627.00 $627 New Fund 0.0% Largest Appropriations

As in previous years, pension and benefit payments and interest and payment of bonds are by far the largest finance general expenses. Advance pension payments, which were reduced substantially in the 2026 budget proposal, are not among the largest expenses this year.

Since the finance general category is entirely locally-funded, local-fund actuals from previous years provide an accurate point of comparison for budgeted versus actual spend. However, the appropriation categories used in the 2022-2024 actuals datasets from the Department of Finance do not correspond exactly to the same appropriation accounts used in the budgets presented by the Office of Budget and Management, meaning an exact line-by-line comparison is not possible.

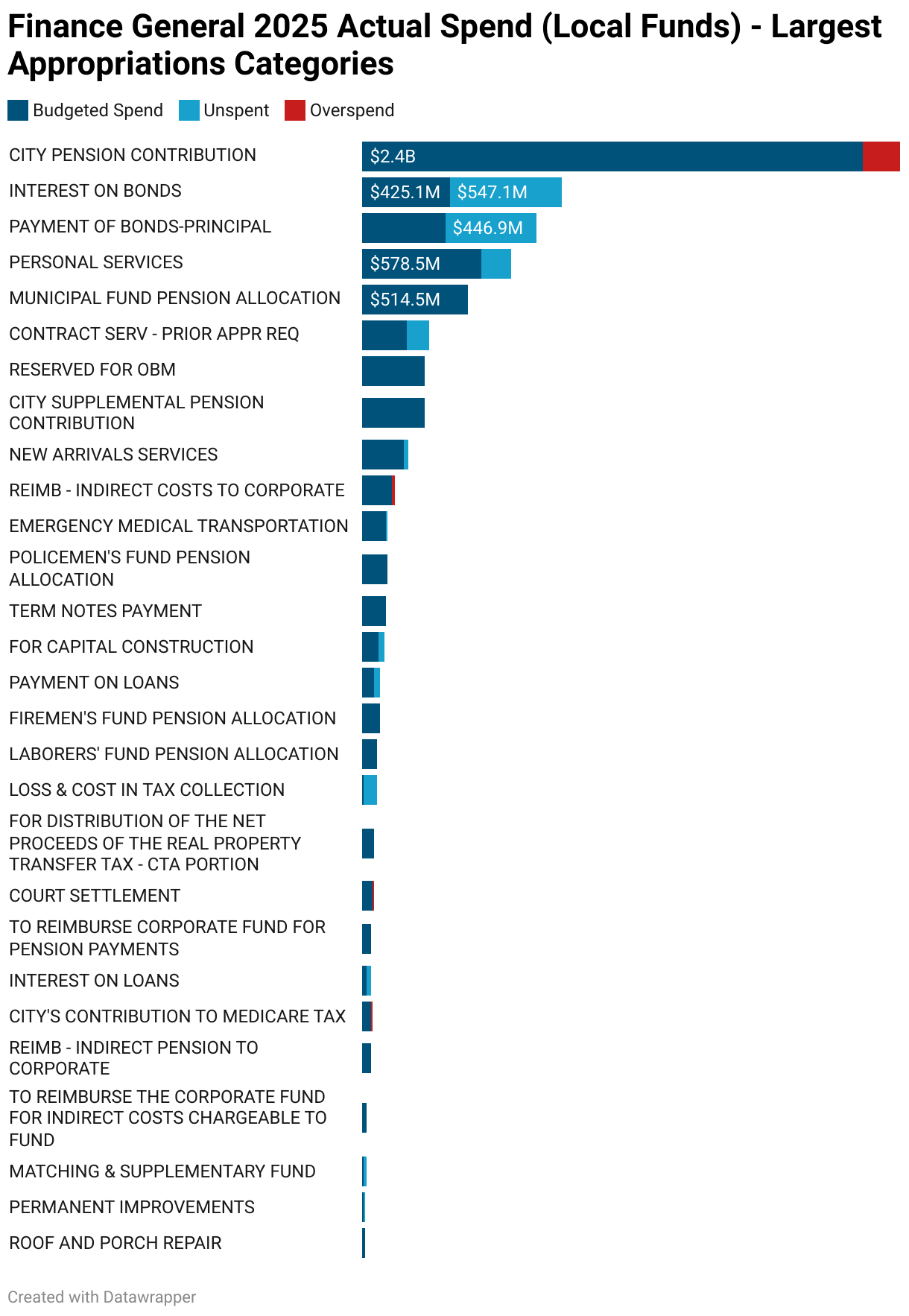

The chart below shows 2024 budgeted spend, unspent funds, and overspend in the largest finance general appropriations categories from the Department of Finance actuals data. Only the largest appropriations are included; the chart is not a comprehensive display of all actual finance general spend.

Finance general actual and encumbered spend exceeded budgeted amounts in the city pension contribution, reimbursement of indirect costs to corporate fund, court settlement, and medicare tax contribution categories.

A small number of finance general appropriations budgeted in 2024 generated no actual spend, including $4.2 million for operations and maintenance reserves, $3.3 million for pension payment reimbursements, and $2.2 million for interest.

APPR. DESCRIPTION Budgeted Spend Unspent OPERATIONS AND MAINTENANCE RESERVE $0 $4,200,000 REIMB - PENSION PAYMENTS $0 $3,327,566 INTEREST $0 $2,200,000 RESTORATION COMMITTEE $0 $500,000 RESERVED FOR EXCESS EXPENSES RELATED TO SNOW EVENTS $0 $500,000 PAYMENT OF CERTIFICATES $0 $100,000 Change from Previous Year

The scheduled wage adjustments appropriation saw the largest net increase from the previous year, up $209.4 million (117.3%) from the 2025 budget. (Recent police and fire contracts have substantially increased the city’s expected salary increases for some of its largest unions.)

Outside contracting costs are up substantially within finance general as well, with the professional and technical services appropriation up $10.4 million (6.7%) from the previous year’s budget, and pass-through spending for delegate agencies up $18.6 million, a very significant 1373.9% increase from 2025. The delegate agencies increase is budgeted from the new Community Safety Fund, which according to Mayor Johnson’s budget address will be funded with a revived corporate head tax.

The largest cuts to finance general appropriations from the previous year are in the advance pension payments, a cumulative -$293.3 across the four annuity and benefit funds. The advance payments have not been eliminated entirely, but are down substantial percentages ranging from -50.3% (policemen's fund) to -66.6% (laborers’ fund).

Among the other largest net reductions in appropriations from the previous years: payment of bonds down -$32.7 million (-4.3%) and interest on bonds -$10.8 million (-1.1%), as well as capital construction down -$12.6 million (-16.1%).

This article first appeared on Better Government Association and is republished here under a Creative Commons Attribution-NoDerivatives 4.0 International License.

Sponsored content

Trending

Housing committee to consider QAP standards changes, Missing Middle sales

Fintech entrepreneur making outsider bid for Chicago mayor

Quigley enters mayor’s race, promising to distinguish as candidate not burdened by future ambitions

Mayor responds to organizers’ call for dedicated city gun violence reduction agency

Mayor proposes $425M in TIF assistance for public infrastructure at The 78 development

What makes up the mayor’s sweeping Residential Landlord and Tenant Ordinance modernization